The price improvement by type of generator

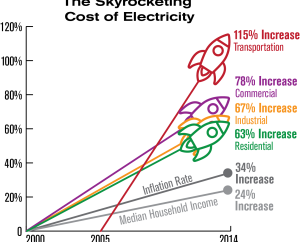

As illustrated first, within the business PPI for 221110 of NAICS there occur two comprehensive indexes that freely track modifications in an Energy Rates for electric ability generation sole for generation of power by non-utilities and the additional for generation of power by utilities. These twice PPIs for the generation of electric power reflect discrepancies in rates by kind of generator. Utility generators affect legacy companies that regulate as vertically incorporated utilities that transmit, develop, and distribute electricity. Utilities persist as major performers in the demand, owning several of the nuclear, huge coal, and hydroelectric capacity plants and are however primarily accountable for the power of electric diffusion. That said, the growth of open admission to communication in 1996, which compelled utilities to arrest fair-market prices to competing producers seeking to stride stability over the utilities’ elevated voltage transmission systems, has overseen development in the stake of energy generated by the type of non-utility energy-producing generators. Various non-utility producers are independent energy builders, which are commonly smaller and are further likely to generate power using non-hydroelectric renewable power and natural gas quotations. Both non-utilities and utilities remember experienced substantial reductions in their aim of coal to produce electric power, with the procedure by utilities lowering from 60.4 percentage in the year 2004 to 32.1 percent 2019; then coal method by independent energy producers decreased from 34.0 percentage in the year 2004 to 13.9 percentage in the year 2019. As examined first, coal has existed replaced with renewable energy and normal gas, with free power inventors more inclined to shift towards renewable power quotations. Independent power builders generated 61.7 percent of their capacity in 2019 from non-hydroelectric renewable energy and natural gas; correlated to 37.3 percentage for utility type. In the exact year, this renewable energy citation credited for 20.1 percent of net production for free power creators, correlated with 2.5 percentage for utilities.

Over this duration, non-utility producers did not raise rates as greatly as utility makers although they demonstrated greater rate volatility. Utilizing annual normal index information, the non-utility chart rose 17.2 percentage from the year 2004 to the year 2019, while the indexing utility rose 41.8%. Around this interval, the utility inventory never fell under its 2004 value, then the non-utility inventory dwindled under its 2004 index value further than the the5thmonth between the 1st month of 2004 and to last month of 2019. This disparity points to the effect that large amounts of existing coal plants remember remembered on utility-based strength generation, while free power inventors with fuel blends that incorporate renewable energy and natural gas have existed able to size goal of falling water prices and improving renewable technology.

Price improvement by provincial fuel mix

This electric power network continues to regionalize. State-founded utilities generally ratify rates, while maximum power expended in a nation arrives from the generating ability in that nation. Using EIA (Energy Information Administration)information and aggregating governments into their pollinations, the PPI policy can correlate price directions across the nations, by mixture fuel. The pictures in this category compare middle price differences in electric residential capacity between countries with low or high capacity lots of the certain fuel categories: natural gas, coal, total renewables (including hydropower), and total renewables (excluding hydropower). In discrepancy, within the central PPI hierarchy NAICS 221122, local PPIs for local electric strength are incorporated to establish and aggregate inventories for overall household electric power.